Fraud Forensic Accounting Firms 2026: Best Options

A practical guide to the best fraud forensic accounting firms in 2026. Learn how investigators trace suspicious transactions, reconstruct financial timelines, analyze fraud evidence, and support legal recovery for businesses and fraud victims.

TL;DR

If fraud losses are real and the evidence is messy, a forensic accounting firm can turn chaos into an investigation file that banks, insurers, and courts respect. Choose based on scope, credentials, evidence handling, and cost breakpoints, not brand heat.

Fraud forensic accounting firms in 2026 are best chosen by fit, not fame. Pick a firm that can preserve evidence, reconstruct transactions, quantify losses, and produce a defensible report for banks, insurers, regulators, or court. Expect hourly rates, retainers, and eDiscovery costs. Recovery depends on timing, documentation, and bank cooperation.

Introduction

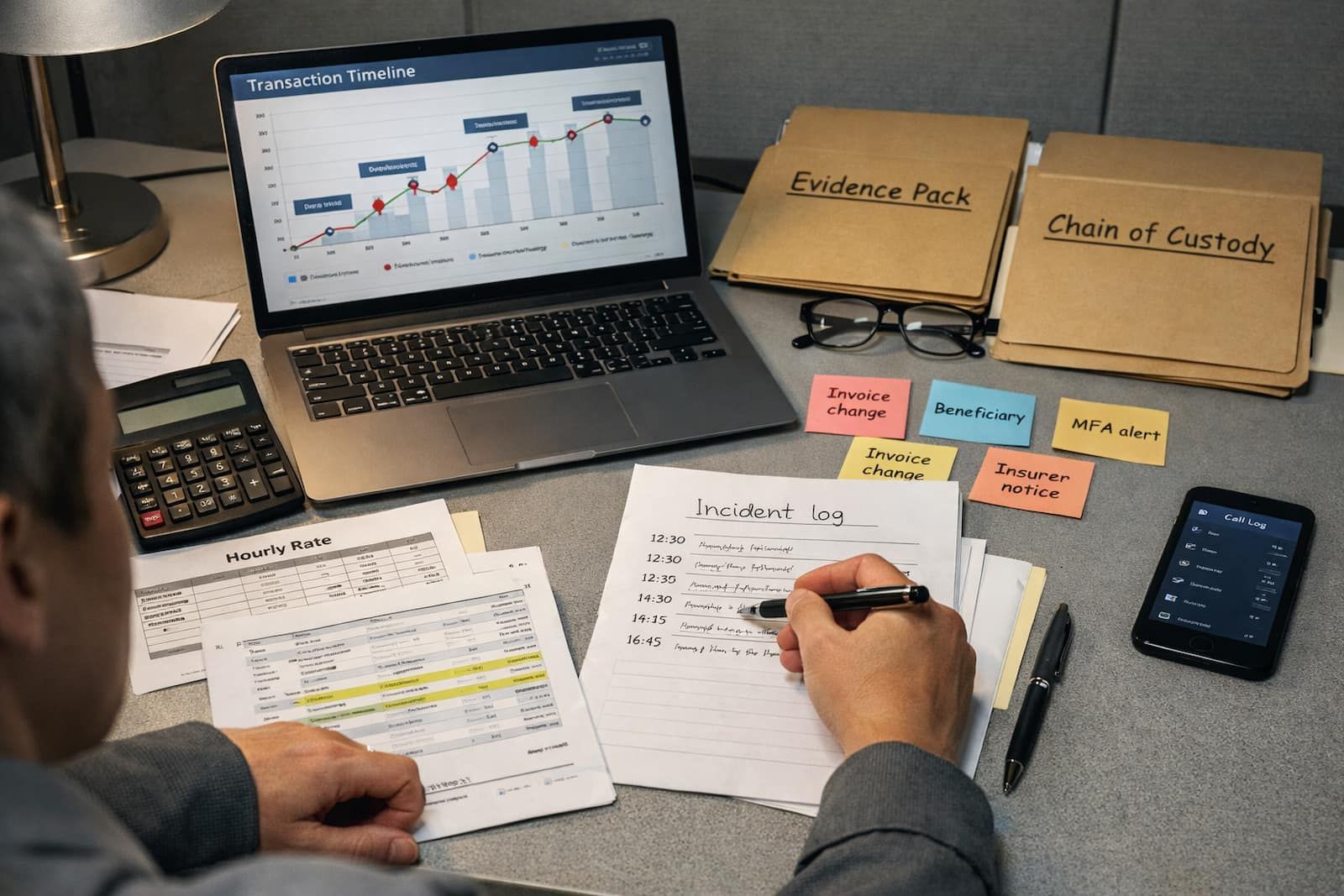

Case file. A real one, in spirit.

USD 148,000 leaves an SMB account via invoice fraud. Two vendor emails. One updated bank details request. The CFO approves. The money is gone in under 20 minutes.

Now the real work starts. The bank wants proof. The insurer wants a timeline. Legal counsel wants numbers that survive cross-examination.

This is where forensic accounting stops being a fancy phrase and becomes an evidence machine.

Jurisdiction clarification: Investigation methods travel. Legal standards and recovery pathways do not. Rules and regulator roles differ across the United States, United Kingdom, Canada, Australia, and New Zealand.

Definition: what a fraud forensic accounting firm actually does

A fraud forensic accounting firm investigates suspected fraud by reconstructing transactions, validating documents, quantifying losses, and producing reports designed to hold up under scrutiny from banks, insurers, regulators, or courts.

Not every accountant is built for that. Some are built for tax. Some are built for audits. Fraud work is different. Fraud fights back.

The 2026 reality: why “best” is a dangerous word

A best firm can still be the wrong firm.

- Some firms are built for expert witness reports and court schedules.

- Some are built for rapid triage and internal controls.

- Some are built for asset tracing across shells and jurisdictions.

- Some are built for eDiscovery and email reconstruction.

- Some are built for board-level investigations with privilege discipline.

A brand name does not replace fit. Fit is what stops you from paying premium rates for a polished PDF that nobody can use.

Scammers love sloppy paperwork. It is their spa day.

Fraud forensic accounting firms 2026: vendor roundup

Below are credible, widely known firms with established forensic, disputes, and investigations practices. Availability, scope, and licensing vary by country and office. Always confirm the actual team assigned.

Quick comparison table (buyer view)

| Firm | Best for | Typical engagement shape | Cost signal | Not a fit when |

|---|---|---|---|---|

| Kroll | Asset tracing, investigations, complex matters | Tracing plus reporting, often multi-jurisdiction | Higher | Loss is small and needs only basic reconciliation |

| FTI Consulting | Disputes, litigation support, expert testimony | Report built for legal scrutiny | Higher | You want a fast operational fix, not a court-ready record |

| Alvarez & Marsal | Large corporate investigations and compliance pressure | Cross-functional teams, remediation heavy | Higher | You only need a narrow fact-find |

| Berkeley Research Group (BRG) | Expert analysis, complex quantification | High-rigor damages and causation analysis | Higher | Case is mostly operational and needs speed over depth |

| BDO | Mid-market investigations, internal control failures | Fraud exam plus process repair | Mid | You need global tracing with aggressive field ops |

| Grant Thornton | Disputes and investigations for mid to large organizations | Structured investigations, reporting | Mid to higher | You need a boutique specialist niche |

| Crowe | Fraud risk, controls, investigations | Investigation plus prevention posture | Mid | You need highly specialized cross-border asset tracing |

| Deloitte | Large-scale forensic, eDiscovery, compliance | Big team, heavy documentation | Higher | Budget is tight and scope is narrow |

| PwC | Complex investigations, dispute services | Enterprise-grade forensics programs | Higher | You need a lean sprint team |

| KPMG / EY | Large org response, governance, regulatory pressure | Investigation plus remediation | Higher | You want a small specialist and fast turnaround |

1) Kroll

Best for: asset tracing, fraud investigations with cross-border elements, complex fact patterns.

Good fit if: funds moved through multiple accounts, entities, or jurisdictions. You need structured tracing plus a defensible narrative.

Not a fit if: the loss is under your cost breakpoint and you need only a short reconciliation.

2) FTI Consulting

Best for: litigation support, disputes, expert witness style work, complex quantification.

Good fit if: legal counsel is already involved. You expect depositions or court timetables.

Not a fit if: you want a lightweight internal review only.

3) Alvarez & Marsal

Best for: corporate investigations tied to operational remediation and crisis response.

Good fit if: leadership wants fix plus proof.

Not a fit if: you only need a tight expert report with minimal remediation.

4) Berkeley Research Group (BRG)

Best for: high-rigor analysis and complex disputes.

Good fit if: the core battle is numbers and methodology.

Not a fit if: the case is mostly evidence collection and operational tracing.

5) BDO

Best for: mid-market investigations, internal controls, employee fraud, vendor fraud.

Good fit if: you want thorough work at a more moderate cost signal.

Not a fit if: you need aggressive field work across multiple countries.

6) Grant Thornton

Best for: investigations and disputes support for mid to large organizations.

Good fit if: you have a defined scope and want disciplined project management.

Not a fit if: you need a narrow niche specialist.

7) Crowe

Best for: fraud risk, investigations, controls, and governance posture.

Good fit if: you want investigation plus control redesign.

Not a fit if: you need global tracing with extensive overseas coordination.

8) Deloitte

Best for: large-scale forensic programs and eDiscovery.

Good fit if: the case has many custodians, emails, and systems, and you need heavy documentation.

Not a fit if: budget is tight and scope is narrow.

9) PwC

Best for: complex investigations and disputes in large organizations.

Good fit if: stakeholders include regulators, insurers, auditors, and legal counsel, and you need deep bench support.

Not a fit if: you want a lean specialist squad and rapid turnaround.

10) KPMG and EY

Best for: investigations tied to governance, risk, and regulatory pressure.

Good fit if: you need investigation plus remediation plan and governance narrative.

Not a fit if: you want a small specialist and fast turnaround.

Selection criteria that actually matters in 2026

Most buyers ask the wrong question. They ask who is best.

Ask these instead.

Evidence handling

- Do they define chain of custody for documents, devices, email exports, and bank statements?

- Can they run a clean eDiscovery workflow, or coordinate with one?

- Do they state sources, limitations, and assumptions clearly?

Scope clarity

Investigation is not a vibe. It is a scoped deliverable.

Litigation posture and privilege discipline

If legal counsel is involved, privilege discipline matters.

Cross-border realism

If funds moved across borders, recovery depends on jurisdiction, bank cooperation, and legal process.

DV Evidence Pack (what to gather before you hire anyone)

- Bank statements for affected accounts, including full transaction detail exports

- Payment confirmations, beneficiary details, and payment reference fields

- Email headers for key emails, not screenshots only

- Invoices, purchase orders, vendor master data records

- Chat logs relevant to approval and changes

- Device logs if available, including MFA prompts and login alerts

- Identity verification steps used by staff, if any

- A written timeline in plain language with timestamps

- Names and roles of approvers and process owners

- Insurance policy and incident notification requirements

Cost math: what forensic work costs and when it is rational

Operational cost table (example math)

| Cost component | Typical range | Example assumption | 30-hour sprint cost | 120-hour case cost |

|---|---|---|---|---|

| Senior forensic lead hourly | USD 350 to 800 | USD 550 | USD 16,500 | USD 66,000 |

| Analyst hourly | USD 150 to 350 | USD 225 | USD 6,750 | USD 27,000 |

| eDiscovery processing | USD 500 to 5,000+ | USD 1,500 | USD 1,500 | USD 4,500 |

| Report and exhibits | Included or extra | USD 3,000 | USD 3,000 | USD 7,500 |

| Total example | Varies | Mix of roles | USD 27,750 | USD 105,000 |

Cost Shock: If the loss is USD 25,000, a USD 30,000 investigation is arithmetic failure.

DV Decision Threshold Triggers

- Under USD 10,000: prioritize bank dispute and evidence preservation.

- USD 10,000 to 75,000: targeted 20 to 40 hour sprint can be rational.

- USD 75,000 to 250,000: full investigation becomes more defensible.

- Over USD 250,000: combine forensic accounting, legal counsel, and controls remediation.

Two micro-scenarios with numbers

Scenario A: Individual authorized payment scam

Loss: USD 12,400.

A full investigation may not be cost-effective. A short expert letter may help in limited cases.

Hard Truth: A report does not create rights. It creates credibility.

Scenario B: SMB invoice fraud with repeat risk

Loss: USD 148,000 and the workflow is still broken.

Prevention value can exceed recovery value.

Escalation framework: severity bands

- Band 1: contained event

- Band 2: material event

- Band 3: business risk event

24-hour rapid action plan (control-first)

- Freeze further loss paths.

- Preserve evidence.

- Notify the bank fraud team.

- Notify the insurer per policy timelines.

- Create an internal incident log.

- Decide the severity band.

- If hiring a firm, send the DV Evidence Pack.

If the loss is material and repeat risk exists, then treat the incident as a business risk event and hire for scope, not brand.

Litigation exposure

If fraud becomes a dispute, documentation becomes discoverable. Stick to facts. Align with legal counsel when litigation is possible.

Psychology neutralization

Fraud uses time pressure, authority theater, and shame. Counter with documentation and calm process.

Prevention difference: individual vs SMB

Individuals need documentation and dispute escalation.

SMBs need repeat-risk reduction plus recovery attempts.

Screenshot checklist

- Beneficiary name, account, and reference fields

- Full transaction detail export

- Email headers

- Vendor master change logs

- MFA prompts and login alerts

- Invoices and change request communications

- Insurer notification proof

- A single-page timeline

Decision framework: branch matrix

- If loss is under breakpoint and facts are clear, then focus on bank and insurer process.

- If loss is material and story is contested, then hire for a scoped forensic sprint.

- If repeat risk exists or insider involvement is plausible, then treat as Band 3.

- If funds moved cross-border or into crypto, then prioritize tracing capability.

FAQ

1) When should we hire a forensic accounting firm for fraud?

When the loss is material, facts are contested, repeat risk exists, or you need a defensible report.

2) Can a forensic accounting firm recover stolen money?

They can support recovery. They cannot force return of funds. Recovery depends on timing, documentation, and bank cooperation.

3) What is the difference between a CPA and a forensic accountant?

Forensic work is investigation method, evidence discipline, and reporting for scrutiny.

4) How long does an investigation take?

A targeted sprint can be 2 to 6 weeks. Complex cases can take months.

5) What should we avoid saying internally during an active fraud matter?

Avoid speculation and unsupported claims in writing.

6) Do we need legal counsel before hiring a forensic firm?

If litigation is likely, counsel helps manage privilege and scope.

7) How do we compare firms beyond brand?

Compare scope discipline, evidence handling, report format, and team experience on your fraud type.

8) What regulators matter across the target regions?

United States: FTC, CFPB. United Kingdom: FCA. Canada: FINTRAC. Australia: ACCC. New Zealand: FMA. These agencies can be relevant for complaint pathways and enforcement context, not as a guarantee of recovery outcomes.

Regulatory citation placeholders (source name only)

- Federal Trade Commission (FTC)

- Consumer Financial Protection Bureau (CFPB)

- Financial Conduct Authority (FCA)

- Financial Transactions and Reports Analysis Centre of Canada (FINTRAC)

- Australian Competition and Consumer Commission (ACCC)

- New Zealand Financial Markets Authority (FMA)

Reviewed for accuracy on 5 March 2026. Standards and regulator guidance can change.

Disclaimer

Educational information only. Not legal advice, accounting advice, or a guarantee of recovery. Engagement suitability depends on facts, jurisdiction, and licensing. Recovery depends on timing, documentation, and bank cooperation.

Fraud logic: loud confidence, weak paperwork.

Write the timeline and preserve the evidence before spending money.