Credit Monitoring vs Identity Theft Protection in 2026: What Helps After Fraud?

Clear breakdown of credit monitoring vs identity theft protection in 2026, explaining what each service actually does after fraud, where they fail, and which steps matter most in the US, UK, Canada, Australia, and New Zealand.

TL;DR

Credit monitoring is a smoke alarm. Loud, late, and not a firefighter. Identity theft protection can help you move faster, but it cannot undo a transfer you authorized. Your real power is freezing credit, locking accounts, documenting everything, and reporting immediately. The “service” is optional. The steps are not.

After fraud, credit monitoring mostly tells you what already happened. Identity theft protection can help with alerts, paperwork, and recovery support, but it still cannot reverse many losses, especially authorized transfers. The best results come from fast action: freeze credit, secure accounts, file reports, and document everything within hours, not days.

Introduction

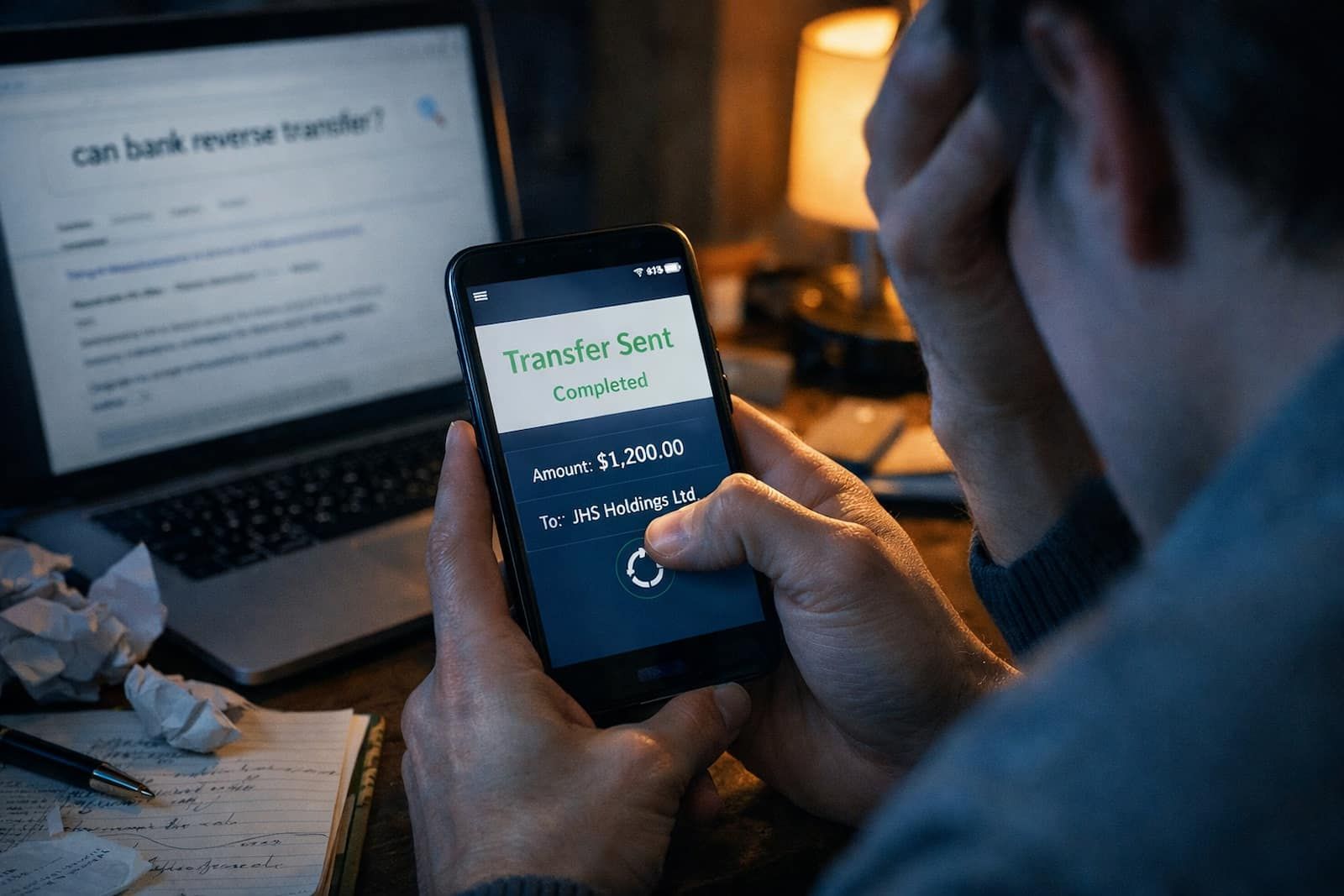

You know that moment. Refreshing the bank app like it is a slot machine. Whispering “please decline” at 2 a.m. Googling “can bank reverse transfer” with one eye open and the other eye screaming.

Here is the truth: sometimes the money is gone. Not “temporarily unavailable.” Gone-gone. And if anyone tries to sell you “guaranteed recovery,” they are either lying or auditioning to become your second scammer.

We are not doing false hope. We are doing damage control. Fast. Ugly. Effective.

“I’m sure the bank can reverse it.”

Bank: “That is adorable.”

Expectation vs Reality

Expectation: “I’ll buy credit monitoring and the bad stuff stops.”

Reality: Monitoring watches the fire. It does not put it out.

Expectation: “Identity theft protection will fix everything.”

Reality: It can help with calls and forms. It cannot time travel.

What Actually Happened

Fraud in 2026 usually lands in one of these buckets:

- Account takeover: A scammer steals a login, SIM swaps you, or bullies support into resetting access. Then they drain funds, change contact info, and lock you out.

- New account fraud: A scammer uses your identity to open credit cards, loans, or phone plans. You find out later, because of course you do.

- Authorized payment scams: You were tricked into sending money, buying gift cards, wiring funds, or paying via crypto. The scammer calls it “verification.” Reality calls it theft with extra steps.

And scammers love scripts. The same recycled lines. The same fake urgency. The same “this is the fraud department” cosplay. They are not masterminds. They are predators running copy-paste theatre.

Scammer script: “Act now or you’ll lose everything.”

Translation: “Act now so I can take everything.”

Why This Issue Happens

After a scam, our brain does something extremely human. It freezes. It bargains. It tries to reverse reality with vibes and refresh buttons.

Shame also shows up fast. Not because you did anything wrong. Because scammers engineer it. Shame keeps people quiet. Quiet keeps scammers paid.

Panic makes us delay. Delay is the scammer’s best employee. Panic also makes us do the worst thing possible: keep talking to the scammer to “fix” it. That is like asking a burglar to help you find your TV.

Light humor, because we need it: the brain after fraud has the processing power of a toaster. We have all been there.

The Moment Money Leaves

Different payment rails have different levels of “maybe” and “nope.”

Credit card

If it is unauthorized, you usually have stronger protections. Dispute processes exist for a reason.

Credit cards have rules. Scammers hate rules.

Debit card and bank transfer (ACH or bank-to-bank)

If it is unauthorized, you may have protections, but speed matters. If it is authorized because you were tricked, banks may treat it as “you approved it.”

Banks are not wizards. There is no “undo” spell.

Wire transfers

Wires can be fast and final. Sometimes a recall works if caught instantly. Often it does not.

A wire is basically “express shipping” for your money to a criminal.

Zelle and other instant transfer services

Used for legitimate transfers. Also used by scammers because it is fast. If you sent it willingly, clawing it back can be brutal.

“Instant” is great until it is instantly gone.

Gift cards and crypto

This is scammer paradise. Recovery is rare.

Gift cards are not currency. They are scammer confetti.

“Is there any way to reverse crypto?”

Sure. Invent time travel. Then call us back.

What You Can Still Control (Step-by-Step Actions)

This is where we stop spiraling and start winning inches back.

Step 1: Stop contact. Block everything.

No more calls. No more texts. No “just one more question.” If the scam is active, you are inside their funnel. Exit now.

Step 2: Secure accounts in this exact order

- Email first. If they control your email, they control resets for everything. Change the password. Turn on MFA using an authenticator app if possible.

- Bank and card logins. Change passwords. Enable MFA. Remove unknown devices.

- Mobile carrier. Ask about SIM swap protection, port-out lock, and recent changes.

- Payment apps. Lock them down. Check linked bank accounts and cards.

Step 3: Freeze your credit

In the United States, freeze with the major credit bureaus. In the UK, Canada, Australia, and New Zealand, use the credit reporting and identity controls available in your country. Freezing is not “extra.” It is the seatbelt.

Step 4: File reports fast and keep receipts

- In the United States:

- Report identity theft at IdentityTheft.gov (FTC).

- Report internet-enabled fraud to FBI IC3, especially larger losses.

- Keep:

- Screenshots (blur sensitive data).

- Transaction IDs.

- Dates, times, names, and call logs.

- Email headers if phishing is involved.

Step 5: Put alerts where they actually matter

- Bank transaction alerts.

- Credit bureau alerts.

- New login alerts for email.

- Address change alerts where possible.

Step 6: Clean up the blast radius

- Replace compromised cards.

- Consider changing account numbers after severe account takeover.

- Check for:

- New payees.

- New forwarding addresses.

- New phone numbers on accounts.

What Banks, Federal Law, or US Regulations Say

In the United States, your protections depend on how the fraud happened and how fast you report it.

- Electronic Fund Transfer Act (Regulation E): Often applies to electronic transfers from consumer accounts. Report quickly, because waiting can limit protections.

- Fair Credit Billing Act (FCBA): Covers many credit card billing disputes for unauthorized charges.

- Fair Credit Reporting Act (FCRA): Drives credit reporting accuracy and dispute rights.

Regulators and reporting bodies to treat as your baseline truth:

- FTC (IdentityTheft.gov): Creates an identity theft report and paper trail.

- CFPB: Explains rights and accepts complaints when financial institutions fail you.

- FBI IC3: Central reporting for internet crime and large-scale fraud.

If someone tells you “the bank must refund it” without asking whether it was an authorized transfer, they are guessing. If someone tells you “refunds are impossible,” they are also guessing. Payment method plus timeline decides most outcomes.

Recovery Timeline

Let us set expectations like adults.

First 24 hours

- You can still stop more damage.

- You might recover funds in some cases.

- You can absolutely reduce the fallout.

This is when you become a part-time detective and a full-time form-filler.

Days 2 to 7

- Disputes start moving.

- Investigations start, slowly.

- You clean up accounts, credit files, and access points.

Weeks 2 to 8

- Some refunds land.

- Some denials land.

- You appeal, escalate, and file complaints when needed.

Months 2 to 12

- New-account fraud can take time to unwind.

- Credit file cleanup can be a slow grind.

- Persistence wins, even when it feels unfair.

“You’ll hear back in 7 to 10 business days.”

“Please do not collapse in our lobby.”

Recovery Scams

If you got scammed once, scammers may circle back like vultures with Wi‑Fi.

Recovery scammers show up as:

- “Hackers” who can retrieve crypto.

- “Chargeback agents” who want upfront fees.

- “Investigators” who ask for remote access.

- “Law firms” with sketchy email addresses and zero credentials.

They will say:

- “We traced the funds.”

- “We just need a deposit.”

- “We can unlock your frozen account.”

They want to steal again. Recovery scams are the sequel nobody asked for. Do not fund the sequel.

Common Mistakes to Avoid

We mess these up because we are in shock. Not because we are “careless.”

- We keep talking to the scammer to “confirm” details.

- We delay reporting because we want to be sure.

- We change passwords but keep the same email compromised.

- We skip the credit freeze because it sounds annoying.

- We pay a recovery scammer because we want the pain to stop.

Detection and Prevention

No fluff. Just practical control.

Detection

- Alerts for transactions and logins.

- Weekly review of bank and card activity.

- Credit report monitoring for new accounts and hard inquiries.

- Device security: updates, reputable antivirus if needed, and no sketchy browser extensions.

Prevention

- Credit freeze as a default if you are not actively applying for credit.

- MFA on email, banking, and payment apps.

- Carrier port-out lock to reduce SIM swap risk.

- Separate email for financial accounts if you can manage it.

- Never “verify” anything by sending money. Ever.

FAQs

Is credit monitoring worth it after identity theft?

Credit monitoring is useful for visibility. It shows new accounts, inquiries, and changes that may signal identity misuse. It does not stop fraud by itself. The real protection comes from credit freezes, account security, and rapid reporting. Monitoring is a dashboard, not a shield.

Do identity theft protection services actually stop fraud?

Some services help by monitoring, alerting, and providing guided recovery support. They can reduce your workload and speed up paperwork. They still cannot prevent every type of fraud, and they cannot guarantee refunds, especially for authorized transfers. Use them as support, not as a substitute for locking down accounts.

What should I do first after a scam in the United States?

Secure email and financial logins, freeze credit, contact your bank, and file reports. Use IdentityTheft.gov for identity theft documentation and FBI IC3 for internet-enabled fraud, especially high losses. Collect screenshots, transaction IDs, and timelines. Speed matters more than perfect wording.

Can my bank refund an authorized transfer if I was scammed?

Sometimes, but it is harder. Banks often treat authorized transfers as customer-approved, even when approval was manipulated. Some institutions have reimbursement policies for certain scam types, and outcomes vary by payment rail and timing. Report immediately, escalate, and file a CFPB complaint if you hit a wall.

How long does identity theft recovery take?

Simple cases can resolve in weeks. New-account fraud and credit file cleanup can take months. The timeline depends on how many accounts were affected, how quickly you froze credit and reported, and how cooperative institutions are. Documentation and persistence shorten the pain, even when it feels slow.

What is the difference between a fraud alert and a credit freeze?

A fraud alert tells lenders to take extra steps to verify identity before issuing credit. A credit freeze restricts access to your credit file, making new credit harder to open in your name. A freeze is stronger. Alerts help. Freezes block.

TL;DR

Credit monitoring tells you the damage. Identity theft protection can help you act faster. Neither one is a magic shield. Freeze credit. Secure email and banking. Report fast. Document everything. Ignore “recovery experts” who want upfront money. Scammers do not get a second bite.

Conclusion

If you are here because fraud hit you, hear this: the scammer is the villain. Full stop. The money may be gone. Your judgment is not. Your next move is still yours.

Lock it down. Report it. Freeze it. Document it. Then let the scammer rot in the sunlight.

If they need you to “verify” anything by paying, it is not security. It is robbery with a script.

Disclaimer

This is education, not a courtroom strategy guide. Do not “wait and see.” Do not “calm down first.” Fraud rewards delay. If money is missing, act now, document everything, and use official reporting channels in your country. If someone promises guaranteed recovery for an upfront fee, congratulations. You found another scammer.